This analysis is written for procurement managers, supply chain leaders, and operations professionals who need a clear picture of where the industry stands in 2026, what forces are reshaping it, and what those forces mean for sourcing decisions. The themes covered: market size and structure, demand drivers, supply chain pressures, sustainability shifts, regulatory changes, and what smarter procurement looks like in this environment.

Key Takeaways

- The U.S. wood pallet manufacturing industry reached an estimated $17.8 billion in 2026 revenue, with sustained growth driven by e-commerce expansion, reshoring investment, and food and beverage sector demand.

- Lumber price volatility and labor constraints remain the dominant cost pressures, translating directly into pallet unit price fluctuations for buyers.

- ISPM-15 enforcement resumed January 1, 2026; international shippers must confirm their suppliers are compliant.

- Single-source pallet dependency is the most common and costly procurement vulnerability in the current market.

- Buyers who use contracts, qualified supplier networks, and total cost thinking consistently outperform those who spot-buy reactively.

Industry Overview: Market Size and 2026 Outlook

A Nearly $18 Billion Industry

According to IBISWorld's 2026 industry analysis, U.S. Wood Pallet & Skid Manufacturing generated an estimated $17.8 billion in revenue in 2026, reflecting a 1.8% revenue CAGR from 2021 through 2026. The industry supports 2,394 businesses nationwide — a count that itself grew at 0.8% annually over the same period.

Pallets are a cyclical, commodity-adjacent product category. Sustained expansion through post-pandemic normalization, lumber market swings, and shifting trade flows signals genuine structural demand — not just a rebound.

Fragmented by Design — and by Risk

The industry is highly fragmented: thousands of manufacturers ranging from small regional mills to larger national players like UFP Industries. No single company controls a dominant share of the market.

For buyers, this fragmentation creates two competing realities:

- Multiple qualified suppliers exist in most regions, creating competitive pricing dynamics

- Small and mid-sized manufacturers carry limited inventory buffers, leaving them vulnerable to capacity crunches during demand surges

- Material shortages can ripple through regional supply chains quickly — with little warning for buyers dependent on a single source

Wood's Durable Market Position

The National Wooden Pallet and Container Association reports that 93% of pallets in the U.S. are made of wood, and more than 90% of all U.S. products move on wooden pallets. Plastic, composite, and metal alternatives exist but remain niche — wood retains dominance because of cost, repairability, recyclability, and raw material availability. That ratio has not shifted materially in years, and no credible near-term displacement of wood is visible in the data.

The 48x40 GMA pallet remains the most common format, accounting for 35% of new wood pallet production and 69% of the recovered/recycled pallet market. Custom and specialty configurations are gaining share, particularly in food manufacturing, pharmaceuticals, and high-compliance retail channels.

Key Demand Drivers Reshaping the Industry in 2026

E-Commerce and Industrial Real Estate Expansion

Warehouse construction is the most direct leading indicator of pallet demand. The 2025–2026 numbers tell the story:

- JLL reported 145.2 million sq. ft. of U.S. industrial leasing in Q1 2026, with 80.7% year-over-year growth in big-box leasing for spaces over 500,000 sq. ft.

- CBRE placed Q1 2026 U.S. industrial vacancy at 6.7% with 249.8 million sq. ft. of total leasing activity

- Prologis reported 47 million sq. ft. of net absorption in Q3 2025 alone, up 64% quarter-over-quarter

Every fulfillment center that opens requires pallets from day one. This volume of new industrial space translates into sustained baseline demand growth for pallet manufacturers.

Reshoring of U.S. Manufacturing

The Reshoring Initiative's 2024 Annual Report documented 244,000 U.S. manufacturing jobs announced through reshoring and foreign direct investment in 2024, bringing the cumulative total since 2010 to more than 2 million jobs. Deloitte reported more than $500 billion in announced U.S. semiconductor manufacturing investment as of mid-2025.

New domestic facilities in electronics, automotive, food processing, and pharmaceuticals all generate recurring pallet demand — volume that previously moved through overseas supply chains. Food manufacturing, in particular, drives some of the highest pallet consumption rates of any sector.

Food and Beverage Sector

Food and beverage is the largest single end-market for wood pallets globally, accounting for over 22% of wood pallet revenue. Domestically, the concentration is even sharper: virtually every food product moving through distribution requires pallets at multiple handoff points.

Skid Management Services' customer base reflects this directly. Active accounts include:

- Knouse Foods

- Campbell Snacks

- Nissin

- Hain Celestial

- Stauffer's

- Plainville

Each represents a food manufacturing operation with continuous, high-volume pallet consumption needs.

Retailer Specification Requirements

Major retailers now enforce detailed pallet specifications that go well beyond basic load-bearing requirements:

- Amazon requires 40x48-inch, four-way access wooden pallets for LTL, FTL, and FCL deliveries

- Walmart Fulfillment Services specifies GMA standard Grade A pallets, 40x48-inch, four-way access, solid wood, under 2,100 lbs, under 72 inches high

These requirements push demand toward Grade A and properly certified pallets — not lower-grade recycled alternatives. For procurement teams, pallet specification has become a compliance requirement with real supply chain consequences if unmet.

Supply Chain Pressures: Lumber Costs, Labor, and Lead Times

Lumber Price Volatility

Pallet pricing tracks lumber markets closely. The BLS Producer Price Index for Wood Container and Pallet Manufacturing (PCU321920321920) moved from 181.4 in December 2025 to 188.7 in April 2026 — a notable acceleration in a four-month window. The commodity-level PPI for Wood Pallets and Pallet Containers (WPU084101) sat at 340.7 in March 2026, reflecting elevated pricing compared to pre-2021 baseline levels.

Pallet-grade lumber moves with the broader softwood market — shaped by Canadian import duties, housing starts, and mill capacity decisions. When framing lumber prices spike, pallet lumber follows, and that cost passes through to buyers fast.

What this means for buyers: Unit price is not stable year-to-year. Buyers who negotiate volume agreements during softer lumber cycles or work with suppliers maintaining diverse lumber sourcing relationships are better insulated from sharp price moves.

Labor Constraints and Automation

Pallet manufacturing is physically demanding work, often located in rural areas, and the labor pool has tightened. BLS data shows employment in Wood Container and Pallet Manufacturing at 67,500 jobs in 2025, down from 69,200 in 2023 — a steady decline even as output demand grew.

Manufacturers are responding with capital investment in automated pallet nailers, board stackers, robotic dismantlers, and sortation equipment. This automation:

- Maintains throughput despite fewer workers

- Reduces per-unit labor cost over time

- Concentrates capacity at better-capitalized facilities

- Improves consistency and reduces defect rates at scale

Production is gradually consolidating toward larger manufacturers. Smaller regional shops with aging equipment face a harder competitive position over the next several years — which affects supply availability, pricing leverage, and long-term relationship stability for buyers who rely on single local sources.

Lead Time Risk

Demand surges create lead time extensions across the supply base. Seasonal food and beverage peaks, retail holiday periods, and post-disruption restocking all strain capacity at the same time. When that happens, single-source buyers have no buffer.

Supply chain managers who have pre-qualified secondary suppliers — or work with a national distributor network — can redirect orders without operational disruption. The mitigation is straightforward:

- Pre-qualify at least one backup supplier before a crunch hits

- Work with suppliers who have network depth, not just local inventory

- Build lead time buffers into seasonal procurement calendars

Sustainability and Regulatory Compliance

What Sustainability Means for Wood Pallets

Wood pallets carry a genuine sustainability story that other materials cannot replicate:

- Virginia Tech research found 95–97% of wooden pallets produced in the U.S. are repaired for reuse, used to repair other pallets, or converted into other products — a recovery rate that plastic alternatives don't approach

- The National Wooden Pallet and Container Association has published an Environmental Product Declaration (EPD) for wooden pallets, validated against data from 85 million pallets, supporting corporate sustainability reporting requirements

- Reconditioned pallet programs — where used pallets are collected, inspected, repaired, and re-entered into the supply chain — are gaining traction among food and CPG buyers with formal ESG commitments

Skid Management Services supplies used and reconditioned pallets alongside new inventory, and offers pallet recycling services for procurement teams with active ESG commitments.

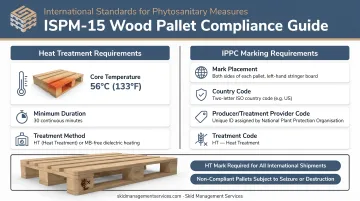

ISPM-15: What Changed January 1, 2026

USDA APHIS confirmed that the suspension of the ISPM-15 hyphen requirement ended December 31, 2025. APHIS and CBP resumed full enforcement January 1, 2026.

ISPM-15 requires wood pallets used in cross-border shipments to be:

- Heat-treated to 56°C for a minimum of 30 minutes throughout the wood

- Properly marked with the IPPC mark, country code, producer/treatment provider code, and treatment type — including the hyphen format between country and producer codes

Any international shipper whose pallet supplier cannot document current ISPM-15 compliance is now exposed to shipment rejections at the border. Enforcement has been active since January 1, 2026, and non-compliant shipments face rejection at customs.

Domestic and State-Level Requirements

ISPM-15 is an international standard, but many large domestic retailers and distributors impose their own pallet quality standards. Separately, state-level environmental regulations affect manufacturers directly:

- North Carolina has banned wooden pallet disposal in municipal solid waste landfills since 2009

- Vermont and other states require air permits for kiln and heat-treatment operations

- California continues to tighten emissions standards affecting wood products manufacturing operations

These regulations vary significantly by state and directly affect manufacturer operating costs. Procurement teams sourcing from multiple regions should account for compliance-driven price differences when comparing supplier quotes.

What 2026 Industry Trends Mean for Procurement Strategy

Treat Pallet Sourcing as a Strategic Function

Lumber volatility, lead time risk, retailer compliance requirements, and ISPM-15 enforcement give pallet procurement decisions real operational and financial weight.

Companies that negotiate annual contracts, lock in pricing during favorable lumber cycles, and pre-qualify multiple suppliers consistently outperform those buying reactively on spot price.

A cheap pallet that arrives late, fails a retailer compliance check, or creates a customs hold at the border is not a cheap pallet.

That kind of strategic discipline also requires the right supplier structure behind it.

Build Resilience Through Supplier Diversification

Single-source dependency — one manufacturer, one region, one price — is the most common vulnerability in pallet procurement. In 2026, there are too many active pressure points for that model to hold reliably:

- Regional capacity crunches during seasonal demand peaks

- Lumber supply tightness in specific markets

- Individual manufacturer labor or equipment constraints

- ISPM-15 documentation gaps from suppliers without robust compliance programs

Working with a national supplier like Skid Management Services reduces this exposure directly. Owned inventory combined with a broad national supplier network means fulfillment doesn't hinge on a single manufacturer's capacity in a given week. For food and beverage accounts — where a pallet shortage can halt a production line within hours — that continuity has measurable cost consequences.

Supplier structure also changes how buyers should think about price — and what "price" actually includes.

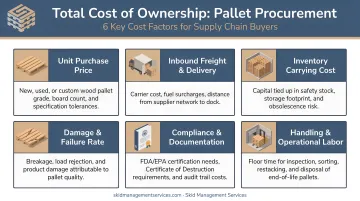

Evaluate Total Cost of Ownership

The true cost of pallet procurement includes:

- Unit price

- Lead time reliability and the cost of production delays

- Damage rates and product loss from sub-spec pallets

- Retailer compliance penalties from non-grade pallets

- Customs costs from non-ISPM-15-compliant materials on international lanes

- Administrative cost of managing supply disruptions

Buyers who optimize on unit price alone often discover these costs during the first demand surge or compliance audit. Building TCO into supplier RFPs and annual contract reviews is the more reliable way to benchmark value — and to justify paying a few cents more per unit for a supplier who actually delivers.

Frequently Asked Questions

How large is the U.S. wood pallet manufacturing industry in 2026?

IBISWorld estimates the U.S. Wood Pallet & Skid Manufacturing industry at approximately $17.8 billion in 2026 revenue, growing at a 1.8% CAGR from 2021 through 2026. The industry has sustained growth through post-pandemic normalization, supported by e-commerce expansion, reshoring investment, and persistent food and beverage demand.

What is driving demand for wood pallets heading into 2026?

The three primary drivers are e-commerce fulfillment expansion (warehouse leasing grew 80.7% year-over-year in big-box categories), reshoring of U.S. manufacturing adding 244,000 jobs in 2024 alone, and sustained high-volume consumption from food and beverage manufacturers who represent the largest single end-market segment.

How do lumber price fluctuations affect pallet costs for buyers?

Pallet-grade lumber is the primary input, so price moves translate directly into unit cost changes — often within weeks. The BLS PPI for Wood Container and Pallet Manufacturing rose steadily from December 2025 through April 2026. Consider volume agreements, forward contracts, or suppliers with diverse lumber sourcing to limit exposure.

What sustainability trends are most relevant to wood pallet buyers in 2026?

Reconditioned pallet programs and closed-loop management are gaining traction among food and CPG buyers with ESG reporting requirements. The NWPCA's EPD — validated on 85 million pallets — provides carbon documentation many sustainability programs require, and 95–97% of U.S. wooden pallets are recovered for reuse or recycling.

What is ISPM-15 and does it affect my pallet purchases?

ISPM-15 requires wood pallets in international shipments to be heat-treated to 56°C for 30 minutes and stamped with a compliant IPPC mark — enforcement of updated requirements resumed January 1, 2026. If you ship internationally, confirm your supplier maintains current certification; non-compliant pallets are subject to customs rejection.

What should procurement managers prioritize when selecting a pallet supplier in 2026?

Focus on four factors: supply reliability, access to multiple manufacturer sources, compliance capability for your shipping lanes, and total cost of ownership. In a market with lumber volatility, seasonal demand surges, and active ISPM-15 enforcement, consistent delivery matters as much as the unit price.