Introduction: The Backbone of Food & Beverage Logistics

Nearly every product on a grocery store shelf traveled on a wood pallet at some point — from the manufacturing floor to a distribution center to the retailer's loading dock. Most consumers never notice. Procurement teams at food and beverage companies notice every day — because supply, cost, and compliance all run through this one material.

The scale is hard to overstate. According to the National Wooden Pallet and Container Association (NWPCA), wood accounts for 93% of all pallets in daily U.S. service, with close to 2 billion pallets in active use nationwide. More than $400 billion in American trade moves annually on wood pallets and containers — making wood the de facto standard for U.S. trade infrastructure.

This guide breaks down what F&B procurement and supply chain teams need to know: market size and growth, why wood holds its dominant position, the demand forces driving volume, key 2026 trends, and supplier evaluation criteria.

Key Takeaways

- Wood holds 93% of the U.S. pallet market and remains the dominant format in food and beverage logistics

- The global pallets market is valued at approximately $92 billion in 2026, growing at 5.2% annually

- Key demand drivers: packaged food growth, online grocery expansion, sustainability requirements, and disruption-driven stocking strategies that took hold after 2020

- Beverages are the fastest-growing application segment within F&B wood packaging

- 2026 priorities: automation-compatible pallet specs, responsible sourcing certifications, RFID traceability, and consolidation toward national suppliers

Why Wood Pallets and Boxes Still Dominate Food & Beverage Packaging

Three practical advantages keep wood dominant across fresh produce, bulk dry goods, beverages, and frozen items — and they hold up under scrutiny.

Structural strength and load flexibility. Standard wood pallets handle thousands of pounds without the flex or failure risk of lighter alternatives. More importantly, they can be built or specified to match the load profile — heavier gauge for bulk beverages, lighter construction for retail-ready consumer goods.

Cost advantage over alternatives. Plastic pallets offer durability benefits, but as Virginia Tech's Center for Packaging and Unit Load Design has noted, they come at a notably higher purchase cost. For high-throughput F&B operations moving millions of pallet loads annually, that gap compounds fast.

Renewable and recyclable. USDA Forest Service data shows U.S. average annual net wood growth runs at roughly 25 billion cubic feet — approximately twice the 13 billion cubic feet removed annually. Wood pallets are not consuming a finite resource. Plastic and metal alternatives, by contrast, are derived from fossil fuels.

There's also a practical lifecycle point that often gets overlooked: a cracked deck board or broken stringer doesn't require a new pallet — it requires common materials and a few minutes. Plastic pallets that fail typically require full replacement, adding cost that accumulates quickly at scale.

NWPCA research indicates that 95% of wooden pallets are recovered and recycled rather than landfilled — reinforcing the total cost argument over plastic.

These structural, economic, and sustainability factors show up clearly in adoption data. NWPCA reports that 95% of pallet-user survey respondents use wooden pallets at their facilities — a near-unanimous preference no alternative material has come close to displacing.

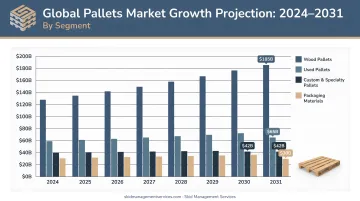

Market Size, Demand, and Growth Outlook

Global and Domestic Market Scale

Two data points frame the opportunity:

| Segment | Baseline | Projected | CAGR |

|---|---|---|---|

| Global Pallets Market (Mordor Intelligence) | $92.11B (2026) | $118.84B (2031) | 5.22% |

| Wood Pallets Market (Grand View Research) | $13.77B (2024) | $17.88B (2030) | 4.5% |

Food and beverage is consistently identified as one of the primary end-use industries driving both trajectories. Within the wood segment, softwood pallets account for over 59% of revenue, and block pallets dominate structural formats at over 69% share.

Mordor Intelligence estimates the global pallets market at $92.11 billion in 2026, projecting growth to $118.84 billion by 2031 at a 5.22% CAGR. Food and beverage is consistently identified as one of the primary end-use industries driving this trajectory.

Two data points frame the opportunity:

| Segment | Baseline | Projected | CAGR |

|---|---|---|---|

| Global Pallets Market (Mordor Intelligence) | $92.11B (2026) | $118.84B (2031) | 5.22% |

| Wood Pallets Market (Grand View Research) | $13.77B (2024) | $17.88B (2030) | 4.5% |

Food and beverage consistently ranks among the primary end-use industries driving both trajectories. Within the wood segment, softwood pallets account for over 59% of revenue, and block pallets dominate structural formats at over 69% share.

Why the U.S. Leads

North America's position in this market traces directly to structural advantages:

- A large, well-developed cold chain and food distribution infrastructure

- High domestic manufacturing output in packaged and processed foods

- Significant export volume requiring compliant wood packaging

According to the NWPCA, more than $400 billion in American trade moves annually on wood pallets and containers. For F&B exporters, ISPM 15-compliant wood packaging is a baseline requirement for clearing international customs.

Supplier Landscape

The competitive landscape spans national and regional players, including:

- Brambles/CHEP — global pooling and pallet rental network

- PalletOne — now part of UFP Industries (~$232M acquisition)

- Kamps, PECO, Millwood, Greif — national and regional distributors

The market has consolidated steadily over the past several years, with national networks expanding through acquisition.

Key Demand Drivers in the F&B Wood Packaging Sector

Multiple converging forces are expanding wood pallet demand across food and beverage supply chains. Five stand out as the primary drivers:

- Packaged food volume growth. U.S. total food spending reached $2.51 trillion in 2025, with food-at-home expenditures at $1.10 trillion. More SKUs, more facilities, and faster inventory turns all increase pallet velocity.

- Online grocery expansion. FMI and NielsenIQ project U.S. online grocery sales will reach $452 billion by 2028, growing at 11.6% annually. Multi-stop DTC fulfillment puts more stress on packaging at every touchpoint — favoring the structural integrity of quality wood pallets.

- ESG and procurement standards. Corporate sustainability commitments are pushing F&B buyers toward biodegradable, renewable materials. Wood meets those requirements in ways plastic alternatives cannot, shifting pallet selection from a default choice to an active procurement preference.

- Supply chain resilience. Post-2020 disruptions exposed the risk of single-source supplier dependency. F&B companies with multi-region operations now actively seek suppliers capable of delivering consistent volume nationally — not just from the nearest regional source.

- FDA FSMA compliance. The Sanitary Transportation rule identifies good-quality pallets as a relevant contamination-prevention measure. Wood pallets are permissible under the Final Rule when properly managed, and for sanitation-sensitive applications, the distinction between new and reconditioned pallets carries real compliance weight.

Market Segmentation: Products, Applications, and Pallet Types

Pallets vs. Wood Boxes and Crates

These are distinct products with different deployment logic:

- Standard wood pallets move full loads through the supply chain — manufacturing, distribution centers, retail receiving docks

- Wood boxes and crates provide individual product protection for fragile or high-value items: bottled beverages, glass containers, specialty foods, and export-packaged goods

Both are relevant to F&B operations, though pallets dominate volume.

Food vs. Beverage Application Segments

Within F&B wood packaging, two application segments drive most of the demand:

- Food applications — fresh produce, frozen goods, bulk dry, and packaged/processed foods — represent the largest volume segment

- Beverage applications — packaged drinks and online beverage delivery — are growing fastest, making this the highest-growth area in the category

New vs. Reconditioned Pallets

F&B buyers regularly face this choice, and the decision carries compliance implications:

| Pallet Type | Typical Application | Key Considerations |

|---|---|---|

| New wood pallets | Sanitation-sensitive, direct food-contact | Clean, untreated, no contamination history |

| Reconditioned/recycled | Secondary packaging, non-contact use | Cost advantage, appropriate for many non-contact logistics flows |

FDA guidance references "good quality pallets" and sanitary controls — there's no universal rule mandating new pallets for all food applications. Procurement teams should evaluate each application's actual contact risk rather than defaulting to one category across the board.

Standard Pallet Formats and Dimensions

The dominant format across both new and reconditioned categories is the GMA 48×40 stringer pallet, rated for a minimum 2,500 lb load capacity. Block pallets are also widely used where four-way forklift entry is required.

NWPCA dimensional tolerances allow +1/4 inch to -1/2 inch on overall size, with a squareness tolerance of 1.5% or 1 inch maximum.

2026 Trends Shaping the Market

Responsible Sourcing Certifications

F&B companies with ESG commitments are asking suppliers to demonstrate FSC or SFI chain-of-custody certification — proof that wood comes from sustainably managed sources. Both standards have distinct scopes:

- FSC chain-of-custody tracks certified forest content from forest to finished product

- SFI's 2022 standard covers certified forest content, certified sourcing, and recycled content

Retail customers are now pushing this requirement down to their suppliers, making certification a procurement differentiator rather than a nice-to-have.

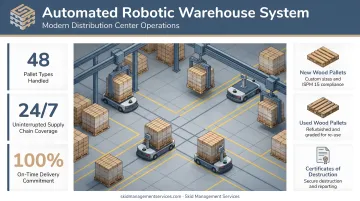

Automation Compatibility

MHI and Deloitte's 2026 industry report found robotics and automation ranked as the second most disruptive supply chain technology, with 39% of respondents rating its impact significant or greater — up 16 percentage points year-over-year. As automated warehousing and robotic handling systems spread through F&B distribution, pallets that deviate from dimensional tolerances cause costly jams and downtime. Suppliers capable of delivering consistent, tightly-spec'd pallets are becoming preferred partners in automated facilities.

RFID and Supply Chain Traceability

FDA's FSMA 204 Food Traceability Final Rule is pushing F&B companies toward faster, more accurate product identification throughout the supply chain. GS1's Serial Shipping Container Code (SSCC) — an 18-digit identifier for logistic units — supports pallet-level tracking for recalls and expiration management. RFID integration with wood pallets remains an emerging rather than standard practice, but procurement teams at larger F&B operations are beginning to ask for it.

Custom Dimensioning for Operational Efficiency

Retailers are tightening shelf and display requirements while F&B operations push to maximize trailer and warehouse cube utilization. Custom-dimensioned pallets have moved from a specialty request to a standard procurement conversation. Skid Management Services supplies custom-size pallets built to specific operational requirements — relevant as more F&B customers optimize pallet configurations for their distribution networks.

National Supplier Consolidation

Multi-facility F&B operations are consolidating from multiple regional pallet suppliers toward national providers who can cover all plant locations under unified pricing and service terms. This reduces administrative complexity and — more importantly — eliminates the regional shortfall risk that became painfully visible during 2020–2022.

Skid Management Services serves this need directly: a national pallet supplier with a broad supplier network covering major F&B brands including Knouse Foods, Campbell Snacks, Nissin, and Hain Celestial Group across multiple plant locations.

What Food & Beverage Companies Should Look for in a Wood Pallet Supplier

Consistent Supply and Geographic Reach

For multi-facility F&B operations, a supplier's network depth matters more than its proximity to any single location. Seasonal harvest cycles, holiday production peaks, and regional weather events all create volume spikes that single-source or regional suppliers often can't absorb.

Key supply continuity factors to assess in any supplier:

- National footprint with owned inventory plus backup supplier network

- Proven ability to scale volume during peak production periods

- Track record serving multi-facility accounts (not just local customers)

Skid Management Services serves major F&B brands — including Campbell Snacks, Knouse Foods, and Nissin — from a model built around owned inventory plus an expansive national supplier network.

Compliance and Specification Capability

Verify these before committing to a supplier relationship:

- ISPM 15 heat treatment for any export-bound shipments — pallets must reach a minimum core temperature of 56°C for 30 minutes and carry the official ISPM 15 stamp

- GMA 48×40 standard inventory for compatibility with most U.S. warehouse and retail systems

- New pallet availability for sanitation-sensitive, direct food-contact applications

- Documentation and certification support for regulated applications

Skid Management Services provides ISPM 15 heat-treated pallets with full stamping and certification documentation — meeting the export compliance requirements that F&B shippers can't afford to get wrong.

Pricing and Total Cost of Ownership

Unit price is the wrong measure. Look beyond it and consider:

- Delivery lead times and reliability

- Ability to scale volume seasonally without penalty pricing

- Whether the supplier offers used/reconditioned options for non-contact secondary applications (reducing cost without compliance compromise)

- Packaging materials availability — corner boards, stretch film, strapping, pallet covers — from the same supplier to simplify procurement

Consolidating pallets and packaging materials under one supplier — as Skid Management Services enables — reduces procurement overhead and eliminates the coordination risk that comes with managing multiple vendor relationships.

Frequently Asked Questions

Are wood pallets in demand in the food and beverage packaging market?

Yes — wood pallets remain the overwhelmingly dominant format, used by 95% of pallet-user facilities according to NWPCA data. The global pallets market is projected to grow from $92 billion in 2026 to nearly $119 billion by 2031, with F&B consistently identified as a primary growth driver.

What are the 2026 trends in the food and beverage wood pallets and packaging market?

The defining trends are: responsible sourcing certifications (FSC/SFI) driven by ESG mandates, automation-compatible pallet specifications for robotic distribution centers, RFID traceability integration linked to FSMA 204 requirements, and F&B procurement consolidation toward national multi-node supplier networks.

What types of wood pallets are most commonly used in food and beverage applications?

The GMA 48×40 stringer pallet is the industry standard — 48 inches by 40 inches, minimum 2,500 lb capacity. Block pallets are common where four-way forklift access is required. Custom sizes exist for specific retailer display requirements, optimized cube configurations, or specialized product types.

What regulations apply to wood pallets used in food and beverage packaging?

ISPM 15 requires heat treatment to 56°C for 30 minutes for any wood packaging used in international trade. FDA's FSMA Sanitary Transportation rule identifies good-quality pallets as part of food contamination prevention. No universal FDA rule mandates new vs. reconditioned pallets, but sanitation-sensitive applications make new pallets the practical standard.

How do wood pallets compare to plastic pallets for food and beverage use?

Wood pallets cost less upfront, are repairable when damaged, and are biodegradable. Plastic pallets offer easier sanitation for direct food-contact applications, but carry significantly higher purchase costs and a fossil-fuel-based footprint that conflicts with ESG procurement goals.

What should food and beverage companies look for when selecting a wood pallet supplier?

Prioritize national supply coverage, ISPM 15 certification capability, GMA standard inventory, and the ability to scale volume with seasonal demand without penalty pricing. A supplier who provides complementary packaging materials under a single account simplifies procurement and cuts vendor management time.